Onboarding & Underwriting Workflow Automation Platform

A single, intelligent platform that consolidates onboarding and underwriting for faster approvals, stronger compliance, and smarter risk management.

Trusted By Leading Enterprises and Partners

Efficiency That Scales

Worth Powers Smoother Onboarding

37%+↑

Increase in Approval Rates

43%+↓

Reduction in Abandonment Rate

350M+

Largest Database of SMBs

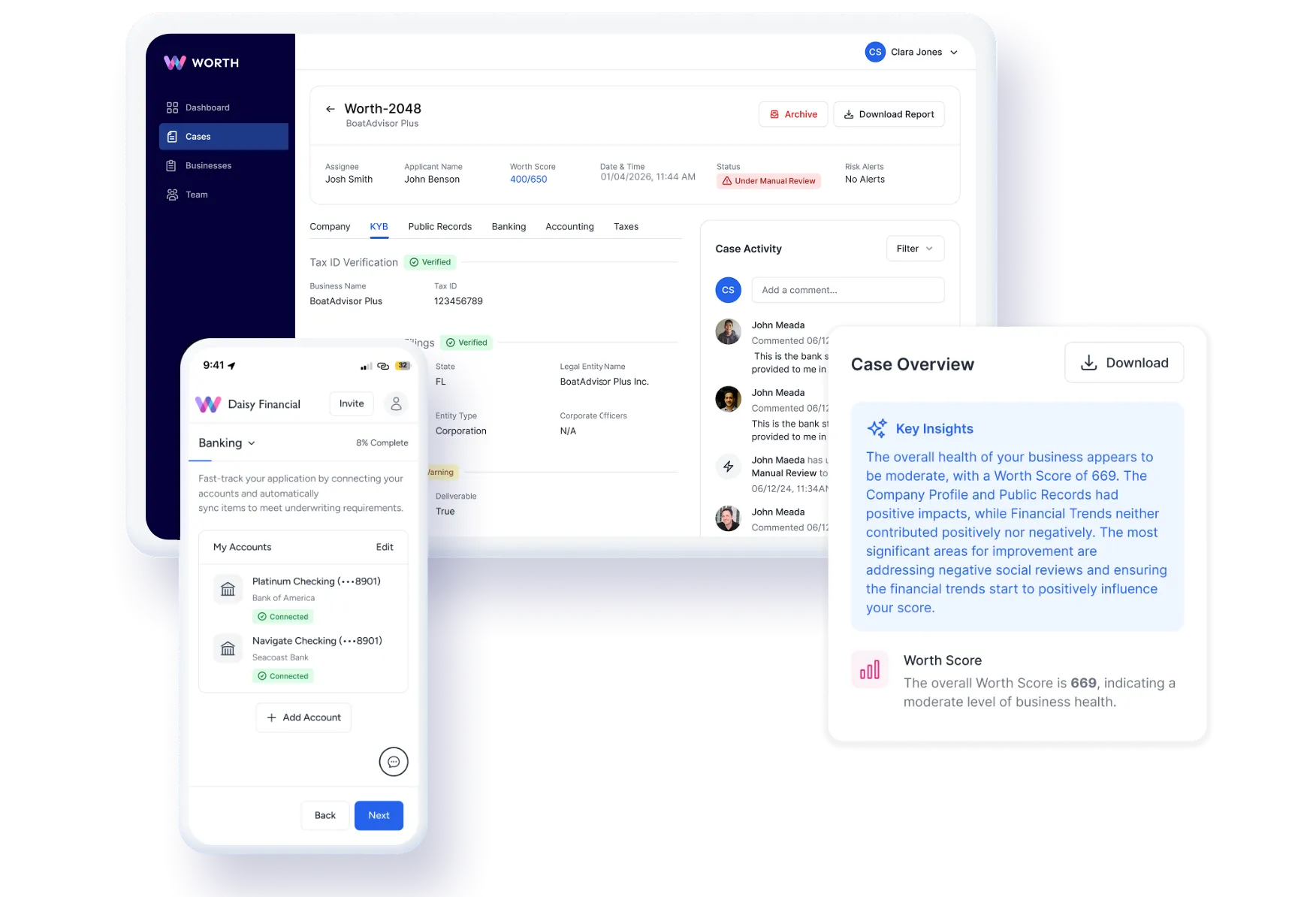

Worth's End-to-End Platform

Our powerful product suite provides everything your team needs to automate onboarding and underwriting, reduce manual effort, and move customers from application to revenue.

%202.avif)

Advanced Features to Accelerate Revenue Growth

Seamless Onboarding

Accelerate onboarding to minutes, optimize customer experience with customized branding and business rules, and ensure high match accuracy to reduce errors and manual intervention.

Learn More

Revenue-Boosting AI Underwriting

Worth's AI synthesizes KYB, KYC, financial, and fraud signals to auto-clear policy-matched cases and route edge cases to underwriters with context already surfaced.

Learn More

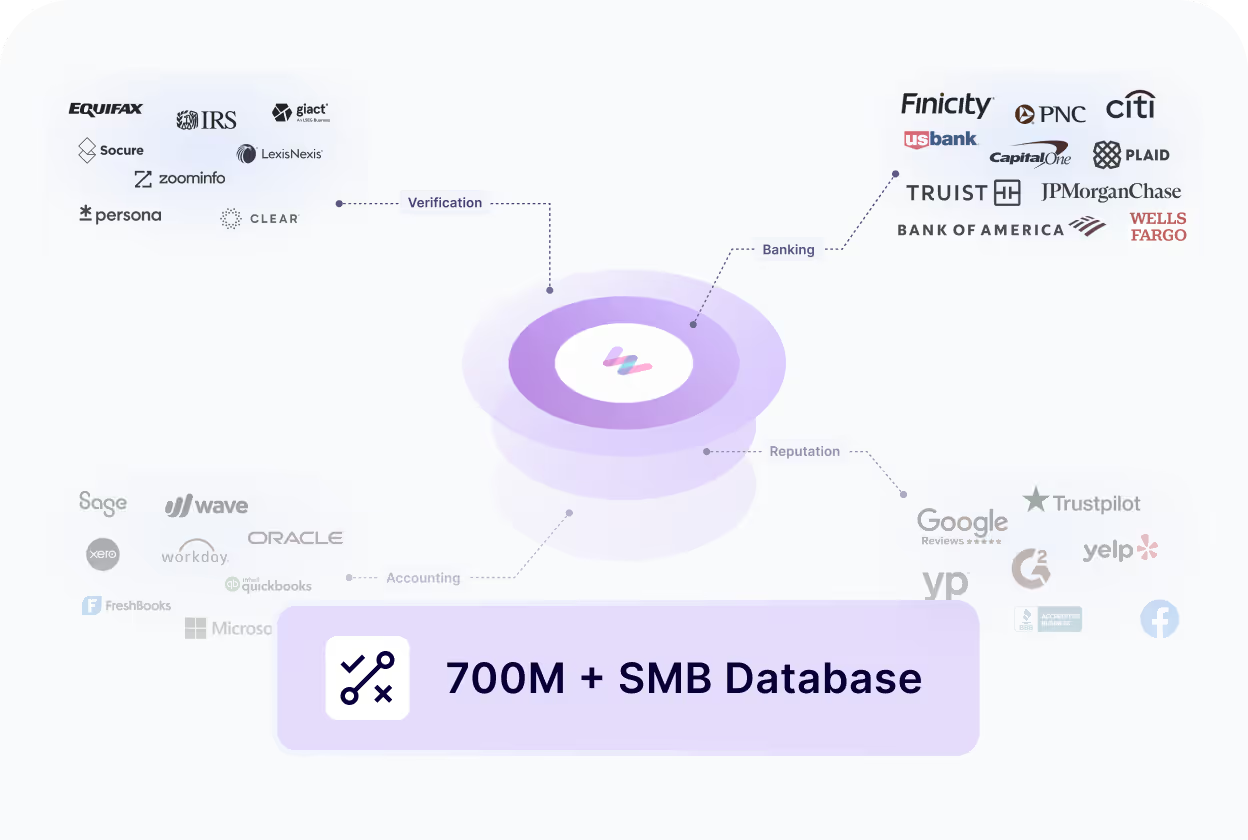

Crosswalking Technology

Inaccurate data slows down onboarding and increases risk. Worth's Crosswalking Technology pulls from SoS, IRS, Google, and dozens of other sources to deliver the industry's most accurate business match rates.

Learn How Crosswalking Works

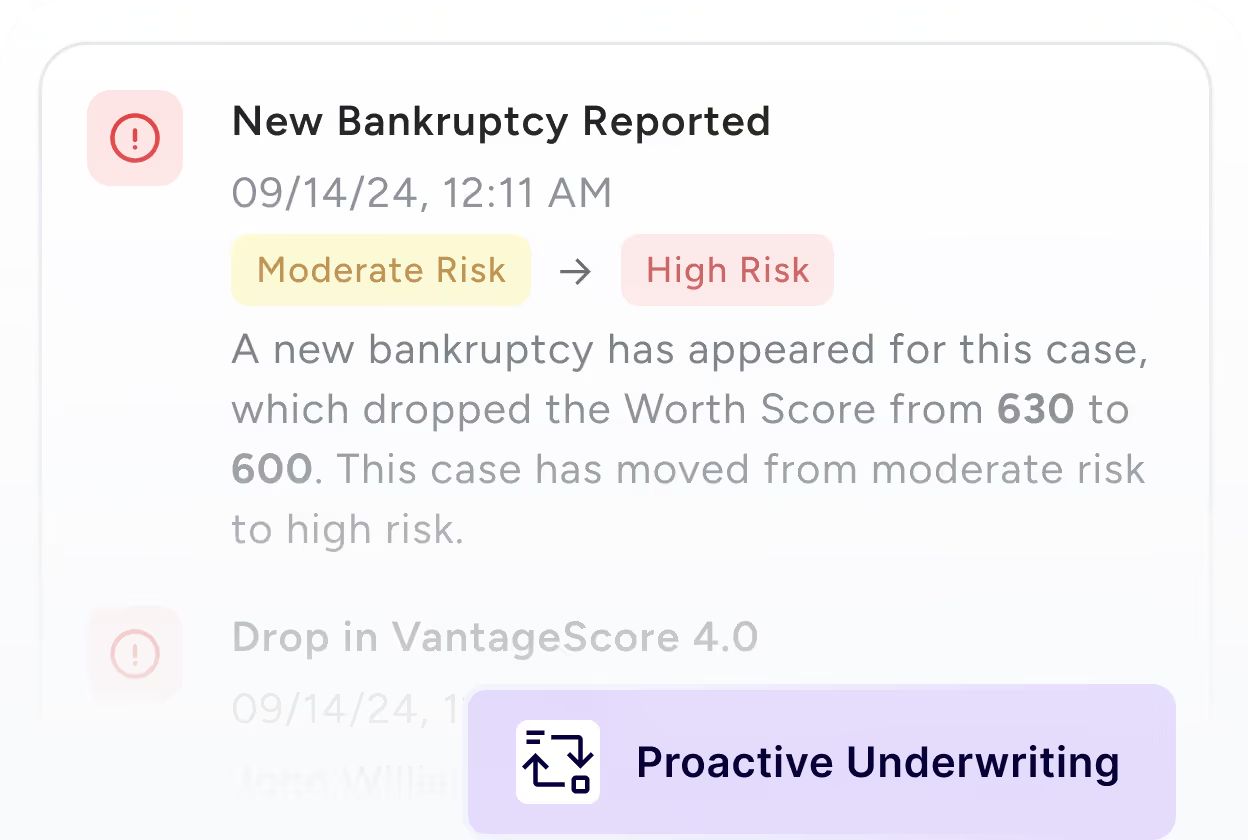

Decision Intelligence

Underwriting wasn’t built for today’s data complexity. While analytics explain the past and AI predicts the future, Decision Intelligence focuses on the next best action. Worth combines verified identity data, risk signals, and decision workflows to enable faster approvals, fewer manual reviews, and stronger fraud prevention.

Explore Decision Intelligence

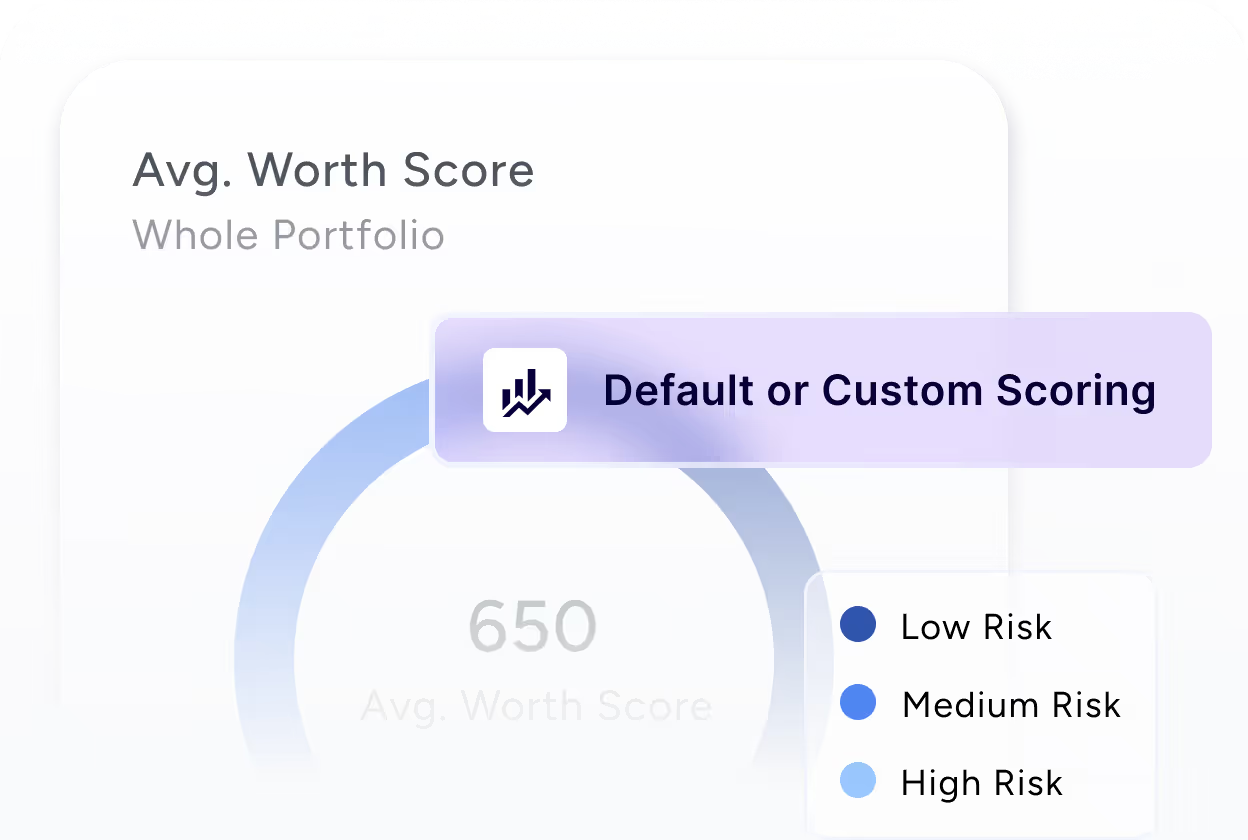

Data Moat

Worth maintains broad coverage across global SMBs, creating a durable data asset that extends beyond one-off API lookups. The platform does more than simply surface records. It resolves inconsistencies, determines what matters, and delivers confidence-weighted outputs that grow stronger with every decision.

Explore Data Moat

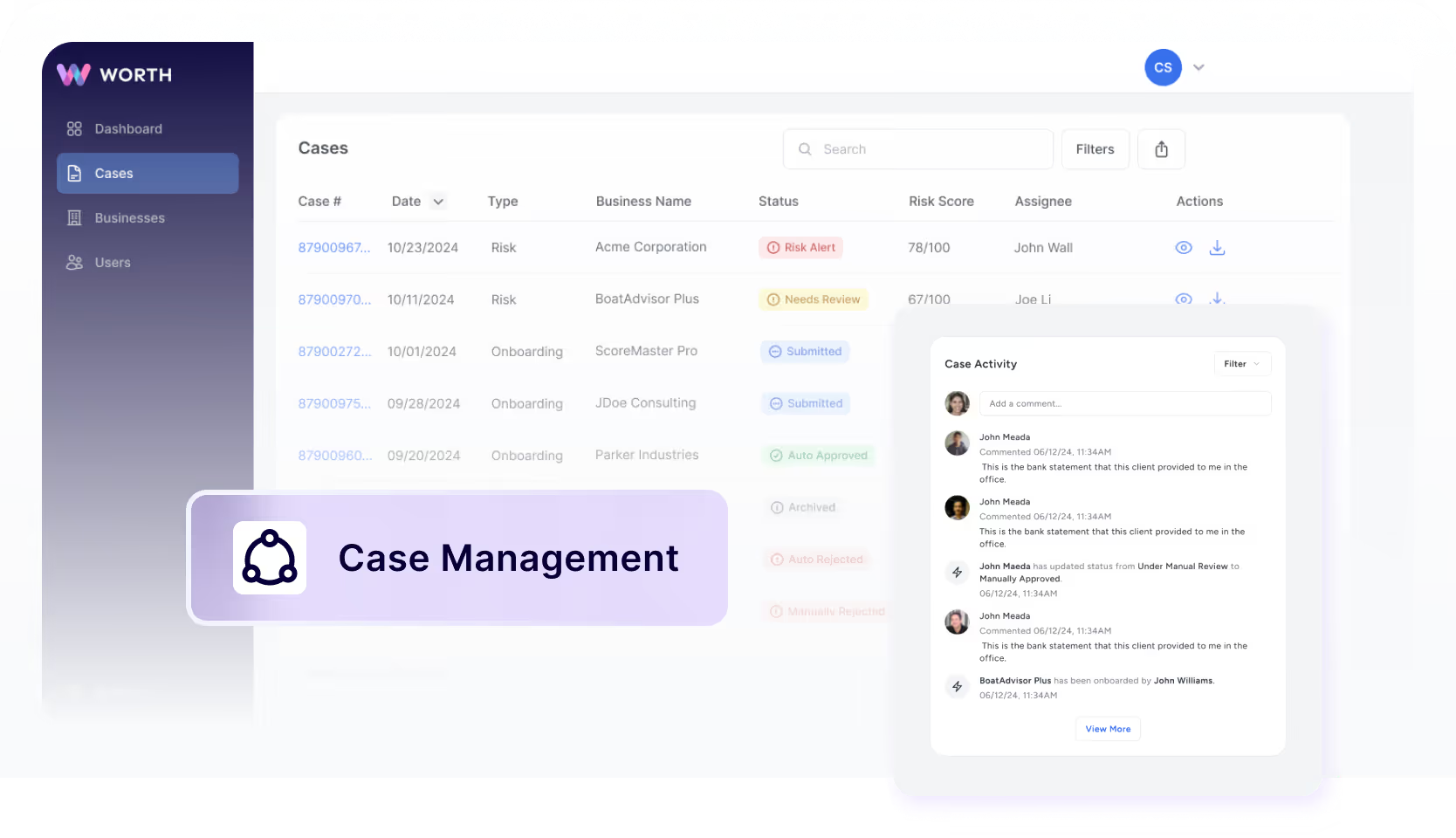

How It Works

The Infrastructure Behind Faster, Smarter Decisions

When onboarding and underwriting run on disconnected systems, your team spends more time managing tools than managing risk.

Worth changes that by consolidating the entire workflow into one platform — automating KYB, KYC, fraud verification, financial checks, and more. With access to a 350M+ SMB database and Worth's proprietary Crosswalking Technology, your underwriters get the full picture they need to make faster, smarter decisions.

Worth changes that by consolidating the entire workflow into one platform — automating KYB, KYC, fraud verification, financial checks, and more. With access to a 350M+ SMB database and Worth's proprietary Crosswalking Technology, your underwriters get the full picture they need to make faster, smarter decisions.

Streamlined Integration

Behind the scenes, Worth orchestrates workflows across systems, minimizing vendor management and allowing your team to focus on building. The platform ensures decisions and processes run smoothly without extra overhead.

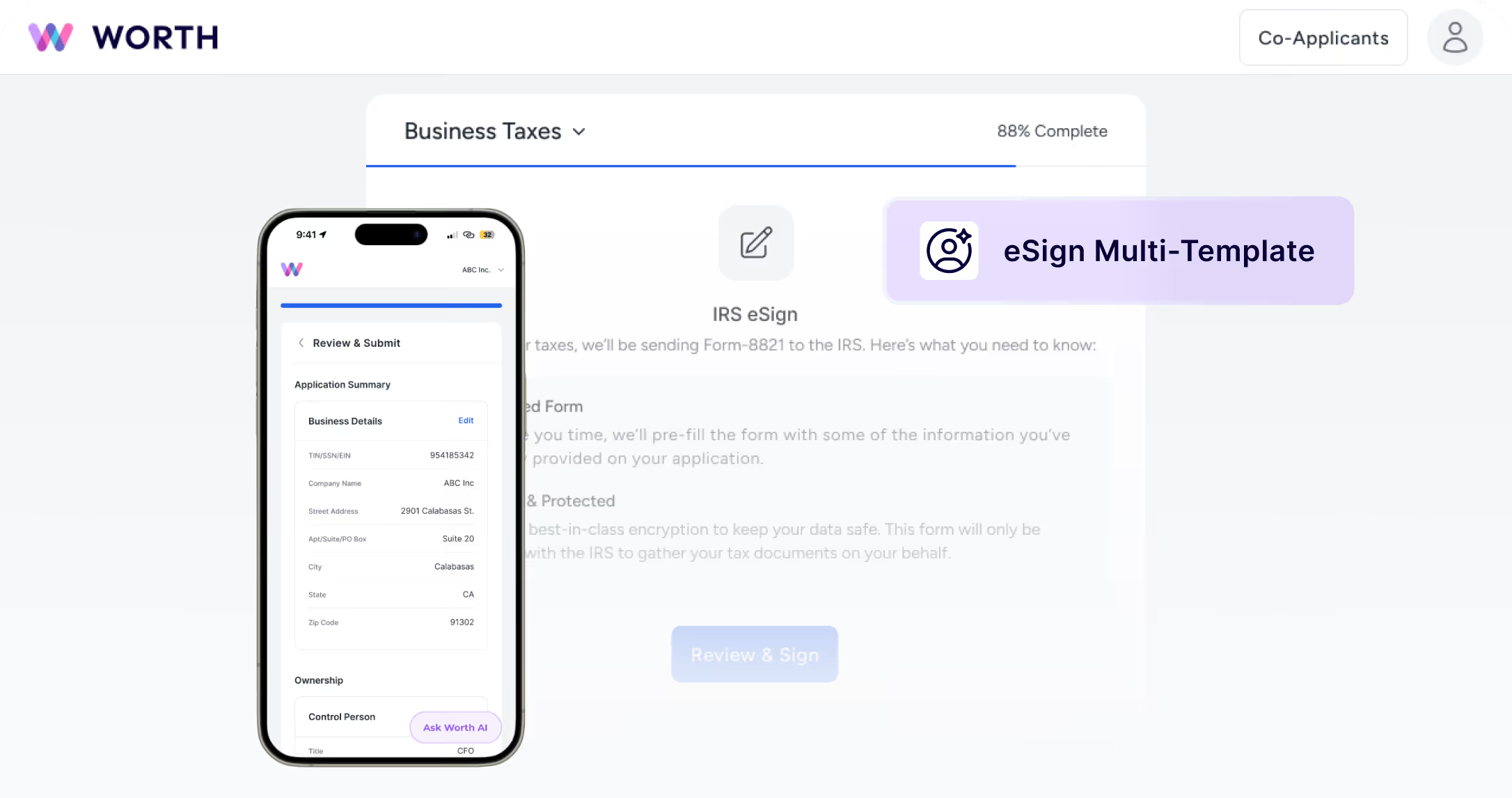

Developer-Ready Tools

Switching platforms shouldn’t mean rebuilding from scratch. Our SDKs and APIs slot cleanly into your existing stack, giving your team flexible, reliable integration tools while keeping the experience seamless and white-labeled for your customers.

International Coverage

Onboard businesses across 200+ countries and territories without adding compliance risk. Worth's international platform handles regulatory checks, ID verification, and fraud prevention — all from one place.

Fully Compliant: SOC 2 & GDPR

Your customers trust you with their data. Worth helps you keep it that way. Our platform is SOC 2 certified and built to meet GDPR, CCPA, and global compliance requirements at enterprise scale.

See Worth in Action

How leading financial institutions move from application to approval faster and with less risk.

Worth eliminates the manual steps, disconnected tools, and compliance gaps that stand between your team and revenue. Built for the scale and complexity of enterprise organizations, Worth brings every part of the onboarding and underwriting workflow into one place — giving you the speed, accuracy, and confidence to make better decisions with less risk.

Schedule a Demo

Built for Institutions That Move Faster

Discover why leading financial insitutions and fintechs choose Worth to streamline onboarding, reduce risk, and accelerate time-to-revenue.

"Leveraging the Worth platform has already been a big win for us. Smarter, data-driven tools help us onboard merchants faster and more reliably while strengthening the connected systems behind our commerce platform."

Greg Snell

SVP & Head of Operational Risk, Priority

"We’re excited about our new merchant onboarding and monitoring tool with Worth, which has already cut our onboarding time by nearly 50%. The result is a smoother experience for medical providers to enroll, who can start offering financing sooner, and a win for patients, who get access to care without delay."

.webp)

Lisa Kesterson

VP, Risk & Lending Operations at PatientFI

"It’s a game-changer. With Worth’s zero-touch onboarding, Aurora can now onboard merchants directly and without handholding."

CPO

Aurora Payments

"From day one, this collaboration has been energizing and highly aligned. Our teams have worked closely and hands-on to build a smarter, more seamless solution focused on an optimized user experience."

Justine Vongxay, CSM

Director, Product Management at VizyPay

Solutions

Industries We Work With

At Worth, we’ve built a platform to meet the demands of today’s most dynamic industries.

Streamline Operations, Maximize Revenue

Consolidate your tools for faster approvals, improved compliance, and smarter risk management.

Schedule a Demo

.webp)